In conversations about public procurement, impact reporting, and organisational strategy, the terms sustainability and social value are often used side by side. Sometimes they’re even used as though they mean the same thing. But while they are related, they are not interchangeable.

Understanding the difference, and how they connect, is especially important for those tasked with creating meaningful change, measuring impact, or commissioning services. And central to that understanding is the role of the Theory of Change.

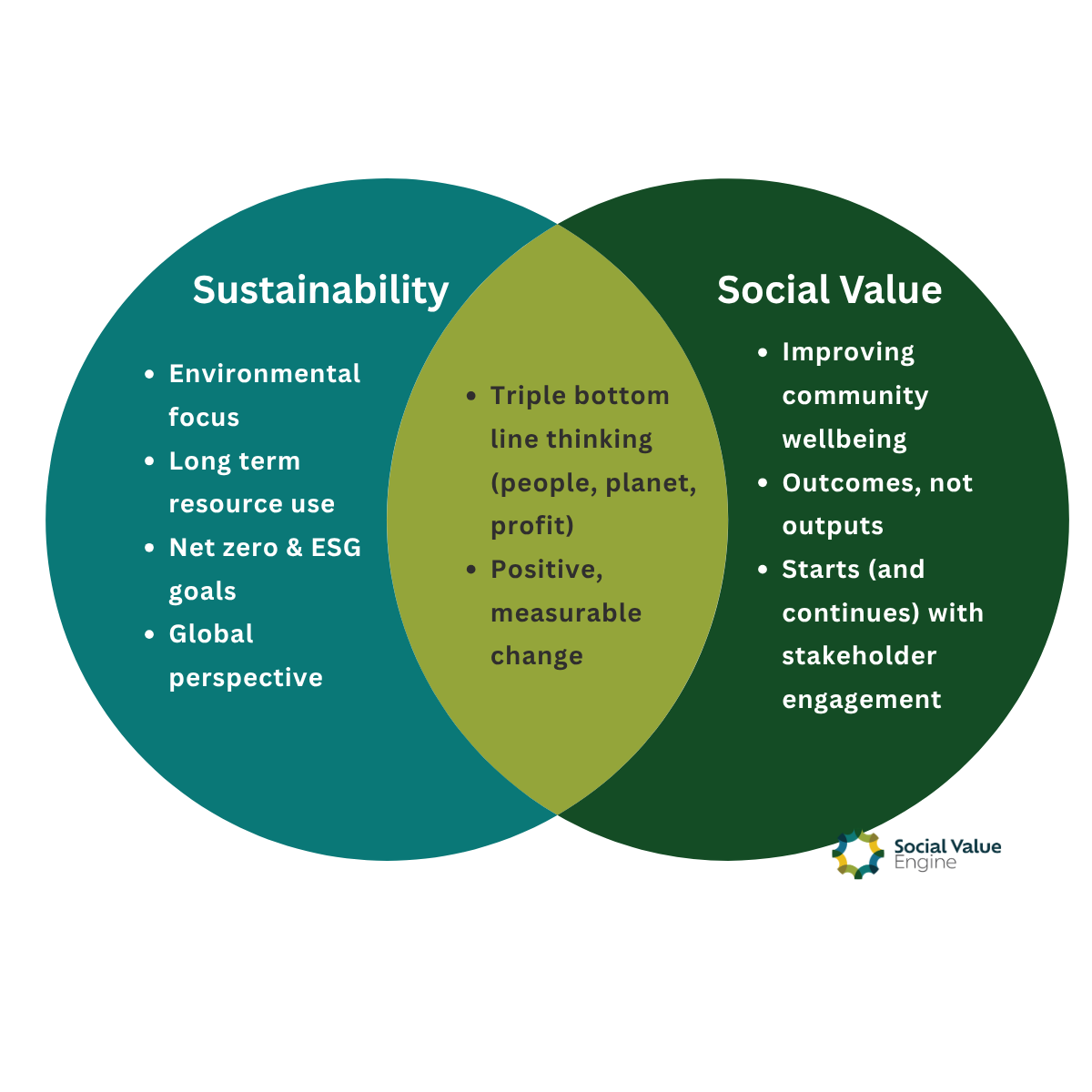

What do we mean by sustainability?

Sustainability is about long-term responsibility. It’s commonly associated with the environment—cutting carbon emissions, protecting biodiversity, reducing waste—but in its broader sense, sustainability also encompasses social and economic resilience. A truly sustainable approach ensures that present actions do not compromise the wellbeing of future generations.

For many organisations, sustainability is embedded through ESG frameworks, net zero strategies, or circular economy principles. It’s about doing less harm, conserving resources, and thinking long term. Importantly, while sustainability may include social outcomes, they are not always the primary focus.

What is social value?

Social value is about the additional benefits that are created for people and communities as a result of a project or investment. It is defined not only by the outputs of a contract, but by the added value it brings beyond the core service.

This could mean creating local employment opportunities, supporting vulnerable groups, improving wellbeing, or strengthening the voluntary and community sector. Social value is people-centred and should be outcome-focused.

The role of the Theory of Change

To meaningfully define and measure social value, many practitioners use a Theory of Change: a structured approach that maps the logical link between activities, outputs, outcomes, and long-term impact. It helps clarify:

Who benefits from an activity

What changes occur for them

Why those changes matter

How you can evidence them

This is where social value clearly distinguishes itself from sustainability. While sustainability can often focus on high-level metrics (e.g. tonnes of CO₂ saved), social value, when guided by a Theory of Change, digs deeper into how lives are improved, for whom, and why it matters in the specific context.

For example, retrofitting homes may be a sustainable intervention, but when seen through a social value lens, its real-world impacts might include reduced fuel poverty, improved mental health, and better educational outcomes for children living in warm homes. The Theory of Change brings this human dimension to the fore.

Where sustainability and social value overlap

The two concepts are not mutually exclusive. In fact, the best initiatives often deliver both. For instance:

A cycling infrastructure project might reduce car emissions (sustainability), while also encouraging active travel and improving access to jobs for those without cars (social value).

A shift to local suppliers might reduce transport miles (sustainability), while supporting small businesses and local employment (social value).

The difference lies in the intent, the measurement, and the framing. Sustainability asks, “Are we protecting future resources?” Social value asks, “Are we improving lives—and can we prove it?”

Why the distinction matters

For commissioners, funders, and impact practitioners, it’s important not to conflate the two. Sustainability alone doesn’t constitute social value. A carbon offsetting scheme, for example, might benefit the environment globally, but may not generate local, measurable outcomes for a specific community.

Likewise, claiming social value requires evidence. A Theory of Change ensures that organisations avoid vague claims and instead make clear, grounded connections between what they do and why it matters.

In procurement, funders want to see impact that’s relevant to local needs, backed by data, and aligned with wider goals like reducing inequality or improving health. Without a Theory of Change, these links risk being superficial or assumed.

Final Thoughts

Sustainability and social value both play vital roles in shaping a better future. But they are not the same. Sustainability focuses on minimising harm and securing long-term environmental and economic resilience. Social value is about creating immediate, positive change for people and communities, backed by a clear rationale and robust evidence.

By applying a Theory of Change can demonstrate not just that they did something, but that it made a difference.